What is the meaning of BRS?

Bank

reconciliation statement is a report which compares the bank balance as per

company's accounting records with the balance stated in the bank statement. It

is normal for a company's bank balance as per accounting records to differ from

the balance as per bank statement due to timing differences.

MeanING; A Bank

reconciliation is a process

that explains the difference between the bankbalance

shown in an organization's bank

statement, as supplied by the bank,

and the corresponding amount shown in the organization's own [accounting]

records at a particular point in time.

CAUSES OF

DISAGREEMENT BETWEEN BANK STATEMENT AND CASH BOOK:

Usually the reasons for the

disagreement are:

1.

That our banker might have

allowed interest which have not yet been entered in our cash book.

2.

That our banker might have

debited our account for any such item as interest on overdraft, commission for collecting

cheque, incidental charges etc., which we have not entered in the cash book.

3.

That some of the cheque which

we drew and for which we credited our bank account prior to the date of

closing, were not presented at the bank and therefore, not debited in the bank

statement.

4.

That some cheques or drafts

which we have paid into bank for collection and for which we debited our bank

account, were not realised within the due date of closing and therefore, not

credited by the bank.

5.

The banker might have credited

our account with amount of a bill of exchange or any other direct payment

into bank and the same may not have been entered in the cash book.

6.

That cheques dishonoured might

have been debited in the bank statement but have not been given effect to in

our books.

HOW TO PREPARE A BANK

RECONCILIATION STATEMENT:

To prepare the bank

reconciliation statement, the following rules may be useful for the students:

1.

Check the cash book receipts

and payments against the bank statement.

2.

Items not ticked on either side

of the cash book will represent those which have not yet passed through the

bank statement.

3.

Make a list of these items.

4.

Items not ticked on either side

of the bank statement will represent those which have not yet been passed

through the cash book.

5.

Make a list of these items.

6.

Adjust the cash book by

recording therein those items which do not appear in it but which are found in

the bank statement, thus computing the correct balance of the cash book.

7.

Prepare the bank reconciliation

statement reconciling the bank statement balance with the correct cash book

balance in either of the following two ways:

(i) First method (Starting with the cash book

balance)

(ii) Second method (Starting with the bank statement balance)

(ii) Second method (Starting with the bank statement balance)

FIRST METHOD

(STARTING WITH THE CASH BOOK BALANCE):

|

(a)

|

If

the cash balance is a debit balance, deduct from it all cheques, drafts etc.,

paid into the bank but not collected and credited by the bank and added to it

all cheques drawn on the bank but not yet presented for payment. The new

balance will agree with bank statement.

|

|

(b)

|

If

the bank balance of the cash book is a credit balance (overdraft), add to it

all cheques, drafts, etc., paid into the bank but not collected by the bank

and deduct from it all cheques drawn on the bank but not yet presented for

payment. The new balance will then agree with the balance of the bank

statement.

|

SECOND METHOD

(STARTING WITH THE BANK STATEMENT BALANCE):

|

(a)

|

If

the bank statement balance is a debit balance (an overdraft), deduct from it

all cheques, drafts, etc., paid into bank but not collected and credited by

the bank and add to it all cheques drawn on the bank but not yet presented

for payment. The new balance will then be agree with the balance of the cash

book.

|

|

(b)

|

If

the bank statement balance is a credit balance (in favor of the depositor),

add to it all cheques, drafts, etc., paid into the bank but not collected and

credited by the bank and deduct from it all cheques drawn on the bank but not

yet presented for payment. The new balance will agree

|

What

are the important things to be remembered while preparing a bank reconciliation

statement?

1. Bank Reconciliation Statement is prepared either by starting with the Bank pass book balance or Cash book balance.

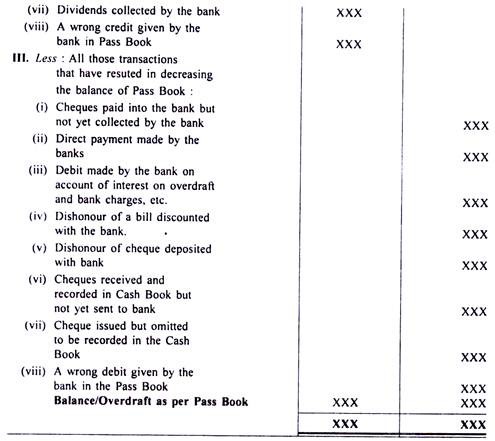

2. If the balance of the Cash book is taken as a starting point then Cash book balance is to be adjusted in accordance with the entries passed in the Bank pass book and vice versa. For example: If the balance is taken as per the Cash book then the following items will be added:

3.Cheques issued but not presented for payment;

4. Amount credited in Passbook but not in Cash book;

5. Deposits made in the bank directly;

6. Wrong credits given by bank;

7. Interest credited in the Passbook.

The following items will be subtracted:

1.Cheques deposited but not cleared;

2. Interest/Bank Charges debited by bank

3.Direct payments made by bank not entered in Cash book

4. Cheques dishonoured not recorded in cash book

5. Wrong debits given by bank

6. If it is prepared with the Bank balance as per the bank passbook, then the above procedure will be reversed i.e the items will be added to the pass book which were deducted from the cash book balance and those items will be deducted from the bank pass book balance which were added to the cash book balance.

OBJECTS/ADVANTAGES/NEEDS/IMPORTANCE/CAUSES

OF PREPARING OF BANK RECONCILIATION STATEMENT

Bank Reconciliation

statement is the basic document of the accounting. Preparation of it is not legally compulsory but by making it,

following objects/advantages/importance

are derived and is needed due to following causes :

(1) To know the accuracy of entries in the Cash Book andlhe Pass Book The

basic object of preparing

Bank Reconciliation Statement is to test the acuracy of causes of difference in

the Cash Book and the Pass Book. The trader tests the accuracy on the basis of

entries in the Cash Book and the Bank ori the

basis of its own transactions.

(2) To know the errors in Cash Book and Pass Book : Cash inflow and outflow must

tally asper, Cash

Book with the Bank Pass Book or,Bank Statement. This brings into focus

errors and irregularities in Cash Book and

Pass Book as well as in the business.

(3) Knowledge of cheques deposited for collection : Bank Reconciliation Statement

gives information about the position of

cheques deposited for collection e.g.,

(i) How many cheques were issued and not presented for payment

up to the date of reconciliation

(ii) How many cheques

were not credited up to the reconciliation time or were dishonored,

(iii) Cause of delay,

in clearance etc

(4) Check on the embezzlement of

cash.: The continuous comparison of Cash Book

with

the Pass

Book keeps check on employees trying to indulge in embezzlement and

misappropriation of funds. The cases of embezzlement of cash by

employees can be

detected easily.

(5) Verification of Bank Balance. The balance of

Bank can be known and it

becomes convenient for

issuing cheques on its basis in future.

(6) Mechanism of

Internal control

: The

preparation of Bank Reconciliation statement is

an important mechanism

of internal control on cash inflow and outflow. It checks

misappropriation of

cheques, bank drafts, malpractices of dishonest employees dealing with

cash and bank etc.

(7) Knowledge of interest allowed by bank or Commission and Interest charged by Bank

The

information regarding transaction of interest and other expenses (e.g.,

commission)

which are recorded by Bank, but

not recorded by customer in his Cash Book is received by

preparation of Bank Reconciliation Statement.

(8) Knowledge of Other

Facts :

(i) The

knowledge of wrong entries by bank;

(ii) The

correct position of cash and bank deposit;

(iii)

Dividend directly collected by bank;

(iv)

Direct deposit of cash or cheque by a debtor;

(v)

Payment made by the bank on

behalf of trader as per

standing instructions;

(vi)

Position of dishonor of bills receivable.

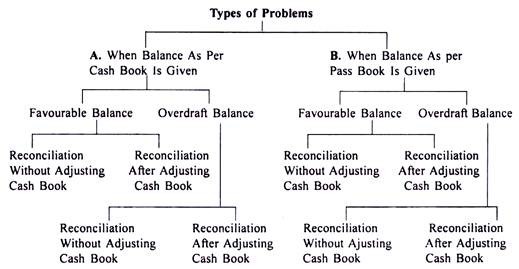

Preparing the Bank Reconciliation Statement (2 Methods)

Here

we detail about the two ways for preparing the bank reconciliation statement,

i.e., (i) Without Adjusting Cash book Balance.

(ii)

After Adjusted Cash Book Balance.

Now we shall move to study the steps taken in preparation of

bank reconciliation statement in each of the above cases.

(I) Preparation of Bank Reconciliation Statement without Adjusting

Cash Book Balance:

Under this approach, the following steps are

to be taken:

Step 1:

All

items appearing in the bank pass book should be checked and ticked with the

items appearing in cash book.

Step 2:

The

un-ticked items in both the books i.e. cash book and pass book are listed

according to their nature of difference.

Step 3:

Put the balance of cash book or pass book as the first

item in bank reconciliation statement. The favourable balance of cash book

(i.e., debit balance) or pass book (i.e., credit balance) is to be shown under

‘plus’ column and unfavourable/overdraft balance of cash book (i.e., credit

balance) or pass book (i.e., debit balance) is to be shown under ‘minus’ column

of the bank reconciliation statement.

Step 4:

All items which have caused the difference between the

balance as per cash book and balance as per pass book are to be examined and

analyzed. In this analysis, the impact of the transactions on the balance as

per cash book should be taken, if starting point is the balance as per pass

book. However, if starting point is the balance as per cash book then the

impact of all transactions on the balance as per pass book should be taken.

Step 5:

The impact of errors and omissions in both the books is

to be analyzed and their affects should be suitably noted in the bank

reconciliation statement. Such errors and omissions may cause decrease/increase

in the balance of cash book or increase/decrease in the balance of pass book.

Errors, that have caused decrease in the balance of cash

book, shall be added, if the starting point is the cash book and vice-versa,

when the starting point is pass book. Similarly, errors that have caused

increase in the balance of cash book shall be deducted, if the starting point

is the cash book and vice-versa when the starting point is the pass book.

Step 6:

The

‘plus’ and ‘minus’ columns are to be balanced.

Step 7:

Put the difference as ‘Balance as per Cash Book/Pass

Book’ or ‘Overdraft Balance as per Cash Book/Pass Book’ as the case may be.

In the above paragraphs, we have discussed the general

points that have to be kept in view while preparing the bank reconciliation

statement. Now, we shall move to discuss some additional and specific steps

required for preparing bank reconciliation statement when:

(A) The starting point is balance as per cash book

(favourable or unfavourable) and

(B) The starting point is balance as per pass book

(favourable or unfavourable).

(A)

When Starting Point Is Balance as Per Cash Book:

If bank reconciliation statement is prepared with the

favourable balance of cash book (i.e., debit balance of cash book) or

unfavourable balance/overdraft balance of cash book (i.e., credit balance of

cash book), the impact of all transactions on the pass book shall be examined.

The transactions shall be

recorded in the bank reconciliation statement as under:

(i) Add: All those transactions that have resulted in increasing the

balance of pass on book.

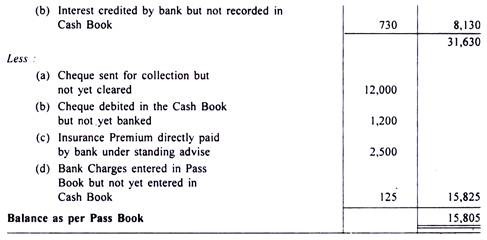

Example:

Cheque issued on 15th March, 2011 but

not presented for payment up to 31st March, 2011 Rs. 10,000.

Impact:

In this

case, the issue of cheque has been recorded in the cash book on the payment

side but it was not entered in the pass book. Therefore, bank balance as shown

by cash book would have been shown at lower than the balance as shown by the

pass book. In other words, the balance shown by the pass book would be higher

than the balance shown by cash book to the extent of that cheque.

(ii) Deduct: All those transactions that have resulted in decreasing

pass book:

Example:

A cheque of Rs. 23,500 received

from Ram Lal, deposited in the bank; however, the bank could not collect the

amount till 31st March, 2011.

Impact:

In this case, the deposit of cheque has been recorded in

the cash book on receipts side but it was not entered in the pass book

Therefore, bank balance as shown by cash book would have been shown at higher

than the balance as shown by the pass book. In other words, the balance shown

by the pass book would be lower than the balance shown by cash book to the

extent of that cheque.

Treatment:

(B)

When Starting Point Is Balance as Per Pass Book:

If bank reconciliation

statement is prepared with the balance of pass book, either favourable (credit)

or overdraft (debit) balance, the impact of all transactions on the cash book

shall be examined.

The transactions shall be

recorded in the bank reconciliation statement as under:

(i) Deduct:

All those transactions that

have resulted in decreasing in the balance as per cash book

Example:

Cheque issued on 15th March, 2011 but

not presented for payment up to 31st March, 2011 Rs. 10,000.

Impact:

In this

case, the issue of cheque has been recorded in the cash book on the payment

side but it was not entered in the pass book. Therefore, bank balance as shown

by cash book would have been shown at lower than the balance as shown by the

pass book. In other words, the balance shown by the pass book would be higher

than the balance shown by cash book to the extent of that cheque.

All those transactions that

have resulted in increasing the balance as per cash book

Example:

A cheque of Rs. 23,500 received from Ram

Lal, deposited in the bank; however, the bank could not collect the amount till

31st March, 2011.

Impact:

In this

case, the deposit of cheque has been recorded in the cash book on receipts side

but it was not entered in the pass book. Therefore, bank balance as shown by

cash book would have been shown at higher than the balance as shown by the pass

book. In other words, the balance shown by the pass book would be lower than

the balance shown by cash book to the extent of that cheque.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Comments

Post a Comment